The New Rules: Delivery Service Providers (DSPs) and Their Contracts

Part 1: How It Started: When DSPs Were Simpler

From a simple, incremental channel, delivery service providers grew into one of the most consequential and complex vendor relationships a multi-unit restaurant brand manages today.

In the Beginning...

It’s not entirely clear why the restaurant industry lagged so far behind travel and retail in evolving into digital businesses. Certainly, something about the complexity of transporting perishable prepared food came into play. Other opinions abound…

- Restaurant products are physical, present, and perishable – unlike an airline seat reservation or a retail product shipped from a warehouse. This means the transaction, fulfillment, and experience all have to happen in the same location.

- Restaurant margins, notoriously thin already, could not tolerate the additional expense that digital transactions and delivery brought to the equation.

- Restaurant people are famously obsessed with hospitality. Apps, screens, and e-payment don’t allow for human interaction, and it was difficult to envision a hospitable experience without that human touch.

- And finally, digital natives play a big part. The consumer base that would ultimately demand digital ordering (millennials, the first generation of true digital natives) had not yet reached its full purchasing power.

- In 2015, millennials surpassed baby boomers as the largest living generation in the U.S.1 Until that tipping point, operators had little market pressure to go digital.

No matter the reason, the fact is that by 2012, when Amazon was already shipping same-day in many markets, fully 50% of independent restaurants in this country did not even have a website.2

When Delivery Was Still Optional

In an environment where the majority of restaurants in the United States did not have a viable digital and delivery business, the emergence of companies that presented themselves as delivery service providers was both slow and tepidly received. Some restaurant brands refused to allow takeout, let alone third-party delivery outright. The idea that an outside company could fulfill an order that originated with a restaurant and take a meaningful cut of the sale was genuinely novel to most operators.

The American consumer evolved ahead of the industry, and demand for delivery found its audience.

A Crowded Field

By the mid-2010s, multiple third-party players were competing for both restaurants and consumers – Grubhub, Postmates, Caviar, Seamless (merged into Grubhub 2013), and a scrappy startup called DoorDash. In this environment, restaurants had the upper hand because this competition among third-party players meant leverage. DSPs were new and unproven, and they had to fight to add restaurants to their marketplaces.

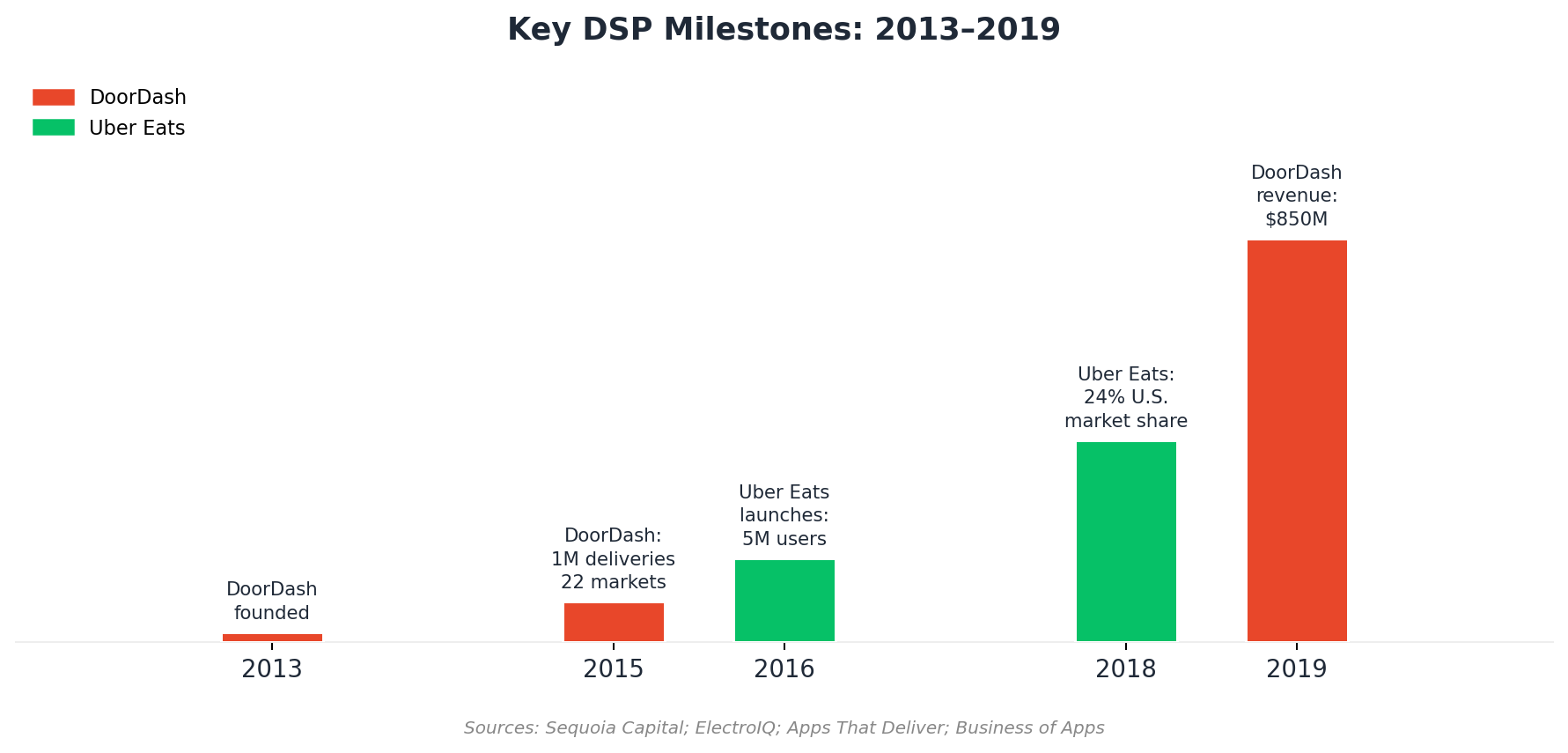

By 2015, the sector was still young and raw. DoorDash had just hit its first 1 million deliveries and operated in 22 U.S. markets.3 Uber Eats didn’t exist yet (it launched in 2016 as "UberFRESH"). Grubhub was the category leader.

At this time, restaurants simply needed DSPs less. Delivery was incremental, not a primary channel. In fact, takeout and delivery were often viewed as a distraction for restaurants, carrying the risk of a negative impact on overall quality and guest experience. The guests ordering on an app were largely new guests for the restaurants, so the economics were defensible — 15-20% commission was easy to rationalize as the cost of customer acquisition.

DSP Contract Negotiations Then

Typically, this meant the negotiation process was simple. A DSP contract in the 2015–2018 era was a short document, often just 2-3 pages, with the primary consideration being the commission rate. Larger brands had some leverage; mostly everyone else took the standard rate.

There were limited marketing commitments, minimal data-sharing complexity, and no subscription tier structures. So, like most other vendor contracts, Legal, IT, or Marketing would handle the DSP contract.

A Different Time

Some data to illustrate the immaturity of the DSP sector in the middle part of the last decade:

- DoorDash: founded in 2013, 1 million deliveries in 2015, operating in 22 markets3

- Uber Eats: launched in 2016, 5 million users by the end of that year4

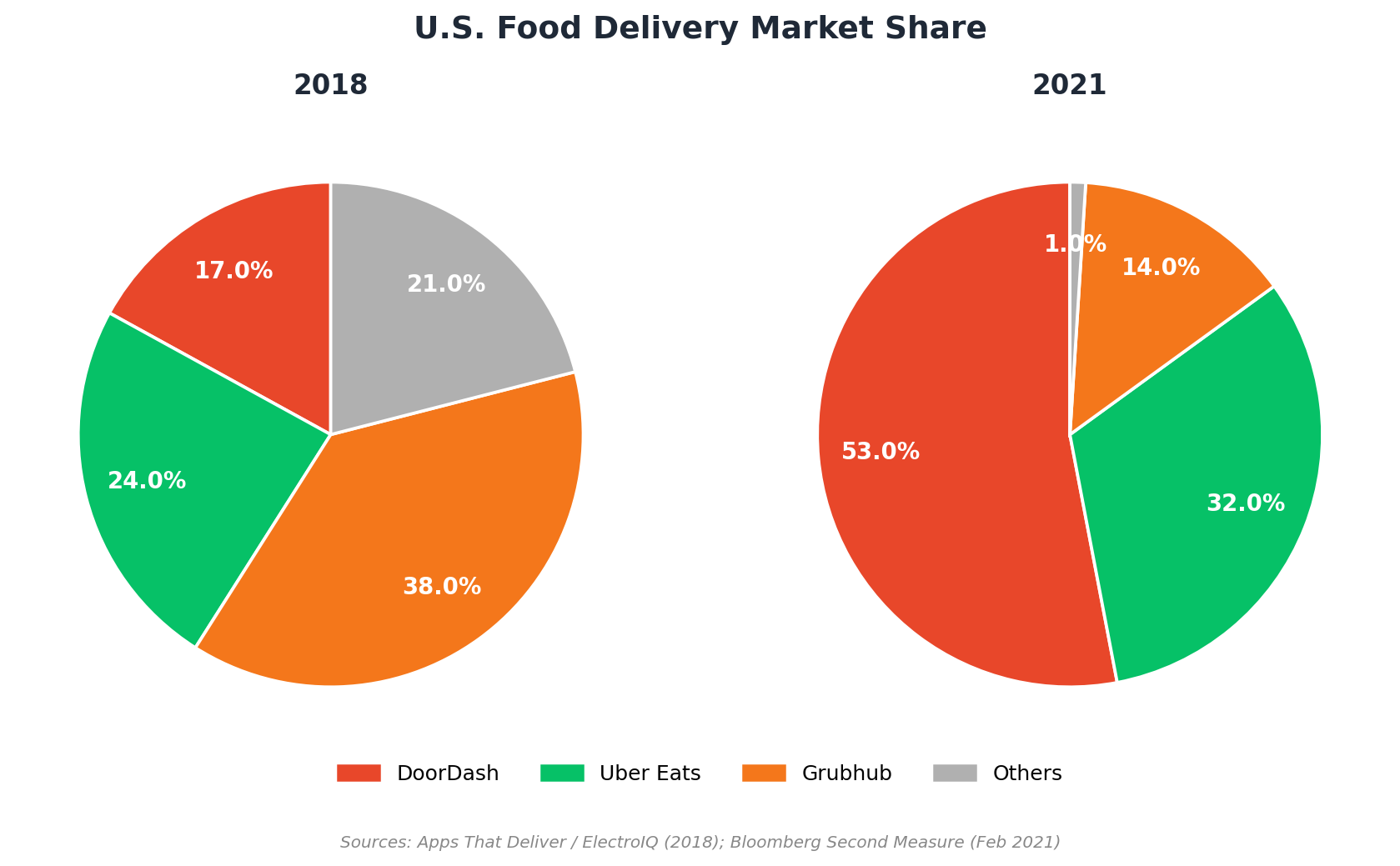

- Market leadership in 2018: Uber Eats held 24% of the U.S. food delivery market; DoorDash was under 20%; Grubhub led5

By early 2019, DoorDash had overtaken Grubhub for the #1 spot by consumer spend. This was a meaningful shift that, at the time, most restaurant operators barely noticed. DoorDash's full-year revenue in 2019 was $850M – respectable but still a small fraction of where it stands today at $14.7B.78

The Birth of a Mindset

The simplicity of the early DSP relationship created habits that would prove costly. When the business was genuinely incremental and the contracts were simple, restaurants signed whatever the DSP sent and rarely revisited the terms at renewal. Auto-renew clauses did the rest, quietly carrying agreements forward year after year - leaving massive sums of money on the table for restaurant leaders.

More critically, there was no thought to align the DSP role with a broader digital strategy

Digital was new to most restaurants, so there was generally no broader digital strategy with which to align. The restaurant industry was still in the earliest stages of e-commerce and online ordering, and DSPs arrived before the strategic framework existed to place them in context.

The result was an organizational pattern that became deeply entrenched. Someone with strategic authority rarely owned DSP relationships. They lived in operations, or marketing, or somewhere in between, were managed reactively and without any real benchmarking, market intelligence, or negotiating experience. This was a rational response to a relationship that genuinely didn't require more attention at the time. The problem is that the relationship changed dramatically, and the mindset didn't. The habits formed between 2015 and 2019 - passive signing, siloed ownership, and incremental thinking - became the default operating posture precisely as DSPs were becoming one of the most consequential and complex vendor relationships in the industry.

Coming Next…

Change was going to happen anyway, and guest demand for e-commerce was inevitable, but a once-in-a-generation disruption would accelerate the restaurant industry’s evolution to digital by more than half a decade. Delivery was about to go from optional to a mandatory, business-saving channel overnight. Part 2 of our series drops next week and will cover the rapid acceleration of food delivery and the resulting scramble for brands of all sizes to keep up.

1 Pew Research Center: “Millennials are the largest generation in the U.S. labor force” (2018).

2 Restaurant Sciences, “Restaurant Internet Marketing Study (RIMS)” (March 2012).

3 Sequoia Capital, “Crucible Moments: DoorDash.” (2024).

4 ElectroIQ, “Uber Eats Statistics By Users, Revenue, Market Share And Facts.” (2026).

5 Apps That Deliver / ElectroIQ. (2021).

6 Fortune, “DoorDash Tops Grubhub” (2019).

7 Business of Apps / ElectroIQ. (2026).

8 DASH Past Revenue Growth / WallStreet Zen. (2026).

Ready to move? Let’s talk.