The New Rules: Delivery Service Providers (DSPs) and Their Contracts

Part 2: How it Changed: The COVID Acceleration

This is the second in a four-part series that tells the story of how the delivery service provider (DSP) category evolved. From a simple, incremental channel it grew into one of the most consequential and complex vendor relationships a multi-unit restaurant brand manages today. The series ends with a clear goal of creating a sustainable framework for DSPs as part of a digital business strategy.

March 15, 2020

- “The list of states requiring restaurants to suspend dine-in service grew by five during the first half of Monday…”

- “... expectations of a nationwide curfew or suspension of dine-in service continue to grow…”

- “...New York, New Jersey and Connecticut joined forces to jointly announce a suspension of dine-in service this morning”

- “Kentucky Gov. Andy Beshear added his state to the rapidly growing list Monday morning. Dine-in service will end for restaurants at 5 p.m.”

- “Last night, New York City, Washington state and Massachusetts all said they would order their restaurants to close for dine-in service Sunday…”

- “Massachusetts Gov. Charlie Baker said he issued an emergency order limiting gatherings to 25 people and prohibiting the on-premise consumption of food or drink at bars and restaurants…”

- “Washington Gov. Jay Inslee said late Sunday he would order all of the state’s bars and restaurants to close for dine-in service…”

The elimination of dine-in flipped the switch overnight. Restaurants that had virtually no takeout or delivery business suddenly needed three things at once: a way for guests to order digitally, a way for that transaction to sync with existing payment systems, and a way to get the food to the door.

The elimination of dine-in flipped the switch overnight. Restaurants that had virtually no takeout or delivery business suddenly needed three things at once: a way for guests to order digitally, a way for that transaction to sync with existing payment systems, and a way to get the food to the door.

The Demand Surge in Numbers

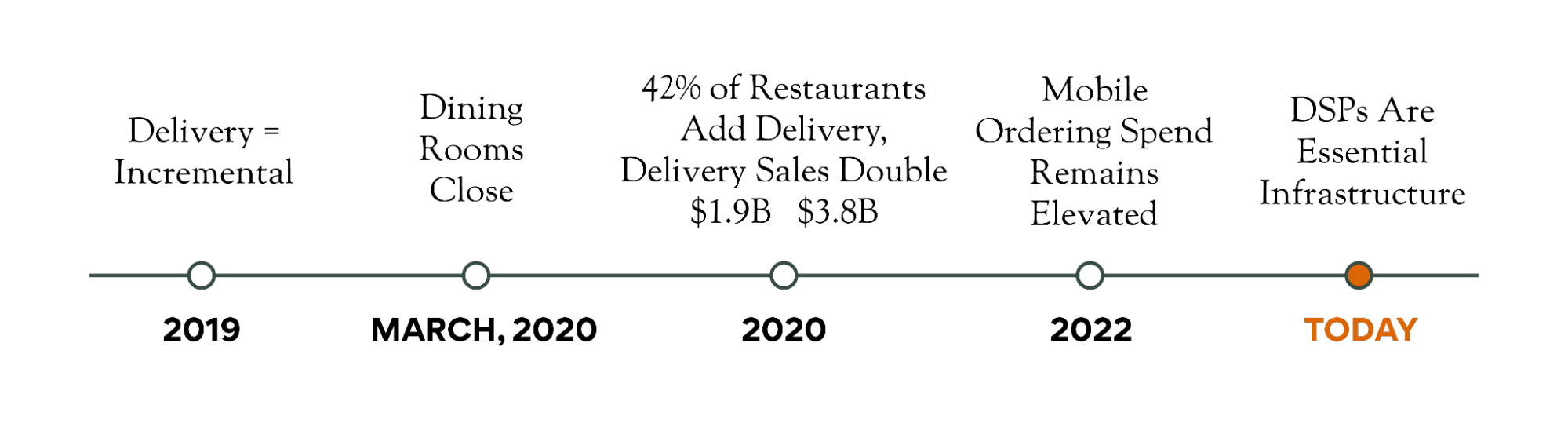

- In three months, delivery sales doubled from $1.9 billion to $3.8 billion.1

- 42% of restaurants added delivery for the first time as a direct result of forced dining room closures

- Nearly half of full-service operators introduced delivery during 20202

- Six in ten guests said post-pandemic, they were more likely to order delivery than before.

The move toward guest demand for food delivery would become a lasting behavioral shift, and restaurants needed to meet that demand.

Though third-party delivery was still in its early stages, it was the most obvious, convenient, and immediate option available. The numbers reflect how quickly restaurants moved: DoorDash grew from 340,000 merchants mid-year to 450,000 by year-end. Grubhub doubled its restaurant listings from 140,000 to 300,000 between Q1 and Q2 alone. By the end of 2020, both DoorDash and Uber Eats would report revenues more than triple their 2019 figures.

The platforms that restaurants had once treated as optional add-ons had just become the industry's primary delivery infrastructure. The DSPs knew exactly what that was worth, and they responded strategically.

And Then the DSPs Got Bigger - Fast

The DSPs didn't just grow with demand. They used the moment to get bigger at the same time that the field narrowed. DoorDash went public in December 2020 and closed its first trading day valued at roughly $39 billion. Uber acquired Postmates. DoorDash bought Caviar. Amazon Restaurants folded. The crowded, competitive field of the mid-2010s was consolidating fast, and the concentration of power that defines the sector today was taking shape.

Permanent Behavioral Change

While restaurants were scrambling to rebuild their digital infrastructure, guest behavior kept evolving. Delivery didn't recede when dining rooms reopened. It embedded itself into daily life, and the platforms facilitating it were simultaneously expanding into something much larger.

DSPs quickly expanded beyond restaurants, adding convenience stores, drug stores, grocery chains, and retail merchants to their platforms. The app was no longer a food delivery tool. It was an on-demand everything platform, and consumers were using it daily for speed, variety, and convenience that no single brand could replicate on its own.

The consequences for restaurants were profound. The marketplace became the destination. Guests who once navigated directly to a restaurant's app or website were now opening a DSP app first, searching by category or specific dish, and choosing from top search results.

What started as a pandemic survival tool had quietly become a permanent feature of consumer life.

DSPs had gone from courting restaurant supply to controlling a channel restaurants could no longer afford to abandon.

The "Incremental" Myth Dies

Pre-pandemic, restaurants could rationalize DSP commissions as a reasonable cost of customer acquisition. The guests ordering through third-party apps were largely new guests, and the math held up. That logic broke down as multi-brand marketplace ordering became ubiquitous. Restaurants' own loyal guests were now ordering through DSPs, which meant DSP revenue was no longer incremental.

It was cannibalizing sales that would have come through owned, more profitable channels. For some brands, DSPs had become a toll road between the restaurant and its own guest.

And that toll was about to get more expensive. The same platforms extracting margin from every sale were building a second revenue stream, this one charging restaurants for the visibility they needed to compete on the very marketplace they were already paying to be part of.

Ordering Platform or Marketing Platform?

The flood of guest activity through delivery apps had a second consequence: the DSPs were accumulating first-party consumer data at scale. And as strategist Eric Seufert observed in his widely-cited 2021 essay "Everything Is an Ad Network," any platform that accumulates sufficient first-party data eventually becomes an advertising platform.

The DSPs followed that pattern precisely. As early as 2019, they began layering paid advertising and sponsored listings into their models, monetizing years of accumulated purchasing behavior. Ordering platforms had become media channels. For restaurants, this created a second dependency. Paying commission on every order was no longer enough. Now they were also paying for visibility and discoverability on the same marketplace they were already paying to be part of. The DSP had gone from delivery partner to landlord, and the rent was going up on two fronts.

Another Pivotal Development

The DSPs also restructured how they charged restaurants for the sales mix they were actively shaping. Subscription programs were marketed aggressively to consumers, and they worked. Subscription transactions became the majority of the sales mix and the fastest-growing segment.

What many restaurant leaders were not aware of was that subscriber transactions carried a higher commission rate than standard marketplace orders, often by 4 to 6 percentage points. The DSPs had quietly introduced two separate commission tiers, and the tier with the higher rate was becoming the dominant one. Restaurants were paying more per transaction on the orders they were getting more of, and many had no idea.

What This Did to Contracts

As DSPs became indispensable and their negotiating position strengthened dramatically. Commission rates climbed, marketing fees expanded, and promotional requirements became more demanding.

Guest data ownership entered the conversation, and so did a new front - DSPs were increasingly powering first-party delivery for restaurant brands, adding another revenue stream and another layer of contract complexity to an already complicated relationship.

The contracts reflected all of it. What had once been a 2 to 3 page document restaurants signed in a matter of days grew into agreements that took weeks and sometimes months to finalize. DSPs showed up prepared. Contract renewal meetings that once involved a rep and a handshake now featured a full team on the DSP side. The brand side was often outnumbered and frequently outmatched.

COMING NEXT…

The anticipated post-pandemic slowdown never came. Guests had been permanently converted. DSPs had permanently expanded. The category had permanently consolidated.

What emerged was a vendor relationship unlike anything the restaurant industry had managed before. No operator building their business in 2015 could have anticipated it, and very few were equipped to navigate it. Part 3 of this series examines the current state of DSP market power: who controls it, how it's structured, and what it actually costs a multi-unit brand to participate today.

1 USDA Economic Research Service. (2024).

2 Restaurant Business Online. (2025).

Ready to move? Let’s talk.