The New Rules: Delivery Service Providers (DSPs) and Their Contracts

Part 3: How It's Going: A Duopoly, a Complex Contract, and a Margin Problem

Two companies now control roughly 90% of all third-party U.S. food delivery orders. DoorDash dominates; Uber Eats is a distant second and fading; everyone else has a significantly smaller portion of the market. That concentration of power, combined with contracts that have grown significantly more complex, means every restaurant brand is negotiating from a position of structural disadvantage - unless they prepare.

The (un)Competitive Landscape

This isn't a competitive marketplace anymore. And when you combine a duopoly (bordering on monopoly) market structure with several dozen contract terms that require active evaluation, and layer in hundreds of millions of dollars in revenue at stake, you get a situation where DSP contract negotiation is, by most measures, the highest-stakes vendor decision a restaurant brand makes.

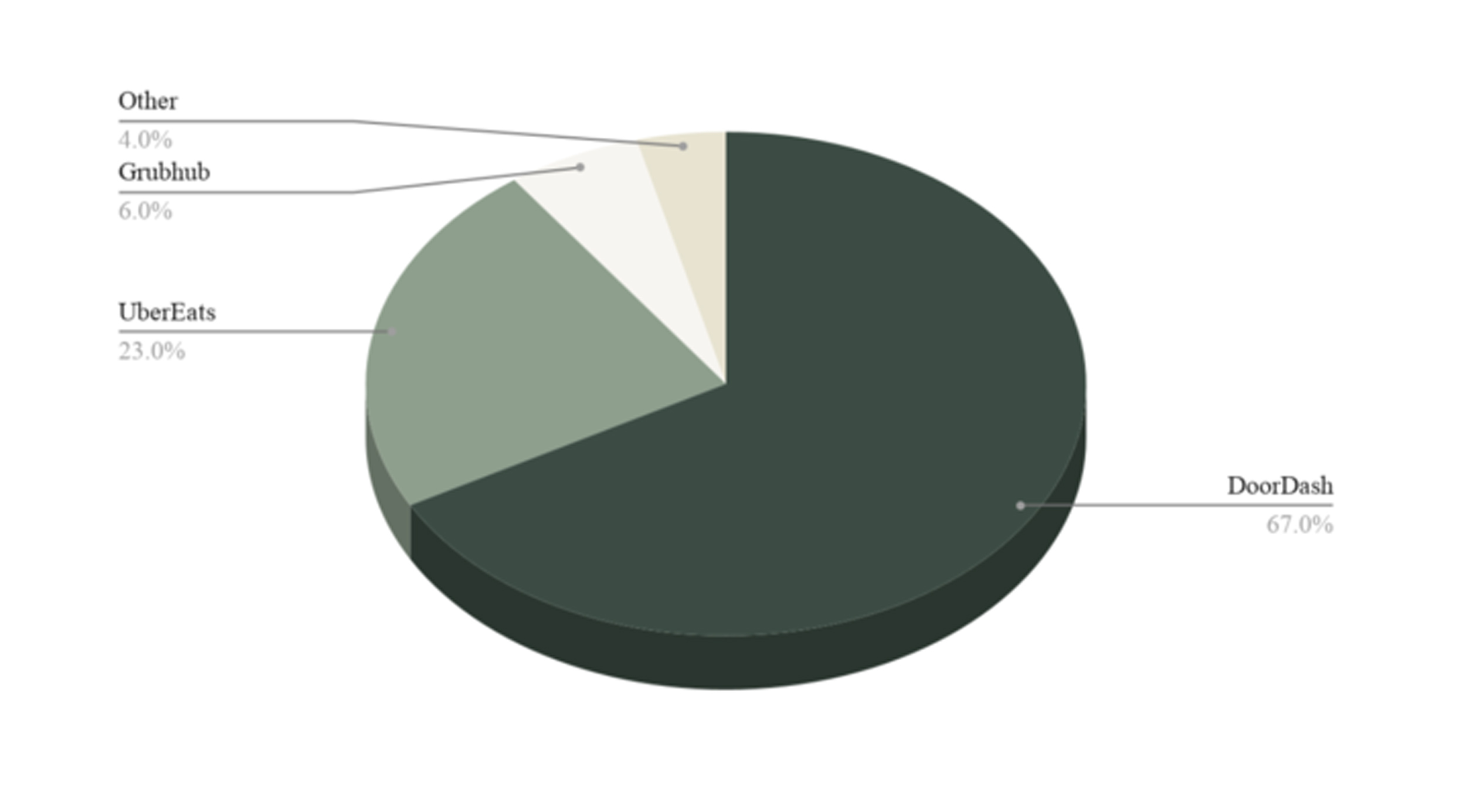

With DoorDash at approximately 67% of the market, and Uber Eats at about 23%, there is no question that the rest of the field is marginal. Grubhub, once the market leader in the mid-2010s, has around 6% of the market and is no longer a meaningful national factor, nor are the other third-tier, regional DSPs.

What this means for restaurants is the “walk away" option is likely non-existent. Revenue from the top two DSPs is a critical part of most brands’ financial models.

Duopoly Becoming Monopoly

Further fueling market dominance by DoorDash is the recent sweeping rate hike announced and implemented by Uber Eats. The industry reaction to this aggressive move was strong, with some brands even vowing to remove themselves from the Uber Eats platform.

On the heels of this development, DoorDash announced Q1 2026 earnings that showed strong growth – 24% increase in gross order value (GOV), and 21% increase in revenue (both figures excluding their acquisition of Dilveroo).

When two companies control nine out of every ten third-party delivery orders, and that may be consolidating further, the DSPs write contracts accordingly. The terms reflect who has the power, and right now, it isn't the brands.

The Contract Has Changed Completely

For years, most brands assumed all they needed to focus on with DSP agreements was the commission rate. That is no longer true.

In our previous article in this series, we discussed DSPs becoming marketing platforms. This means that, fundamentally, a DSP commission now pays for two things: the cost of delivery and the cost of marketing. That dynamic introduces literally dozens of combinations of terms, rates, and commitments and the stakes behind each one are real.

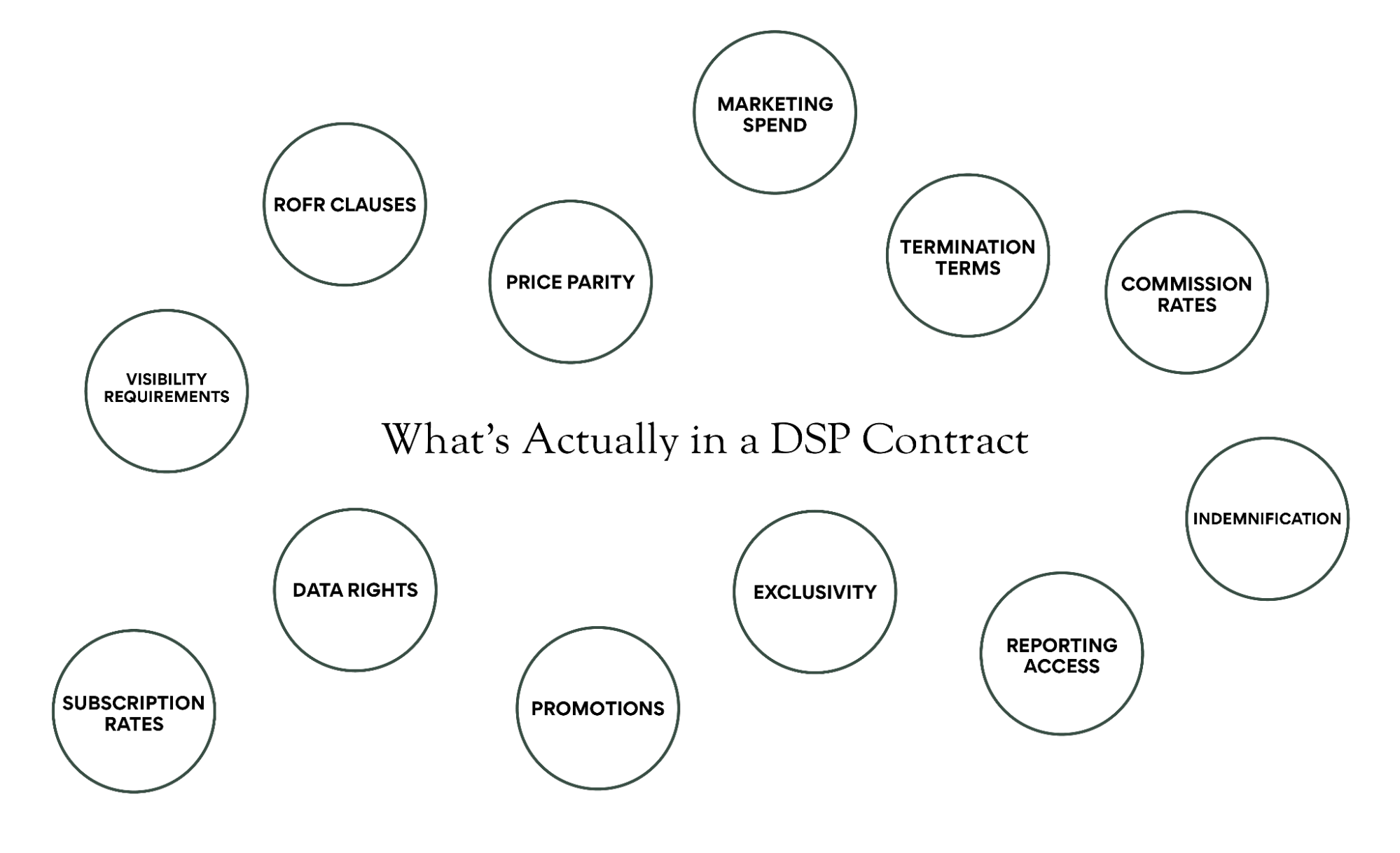

The most direct hit to the P&L comes from fee structure and marketing obligations. Subscription commission rates run meaningfully higher than marketplace rates, and brands are increasingly required to fund promotions and discounts on top of that. Meanwhile, DSPs are requiring higher minimum marketing spend commitments as a condition of meaningful visibility — and non-participation carries a volume penalty.

The terms with longer-term consequences are harder to see in the moment. Data rights provisions determine whether a brand ever learns who its DSP customers are. Exclusivity and right-of-first-refusal clauses can bring discounts for the brand yet restrict future partnerships or channel decisions. Price parity requirements impact the brands ability to offset commissions with markups. And indemnification and termination language tend to be an afterthought, but are important parts of the contract about which the brand should have a voice in the conversation.

Every one of these terms is negotiable, but only if a brand knows to ask.

The Price of the Platforms Continues to Rise

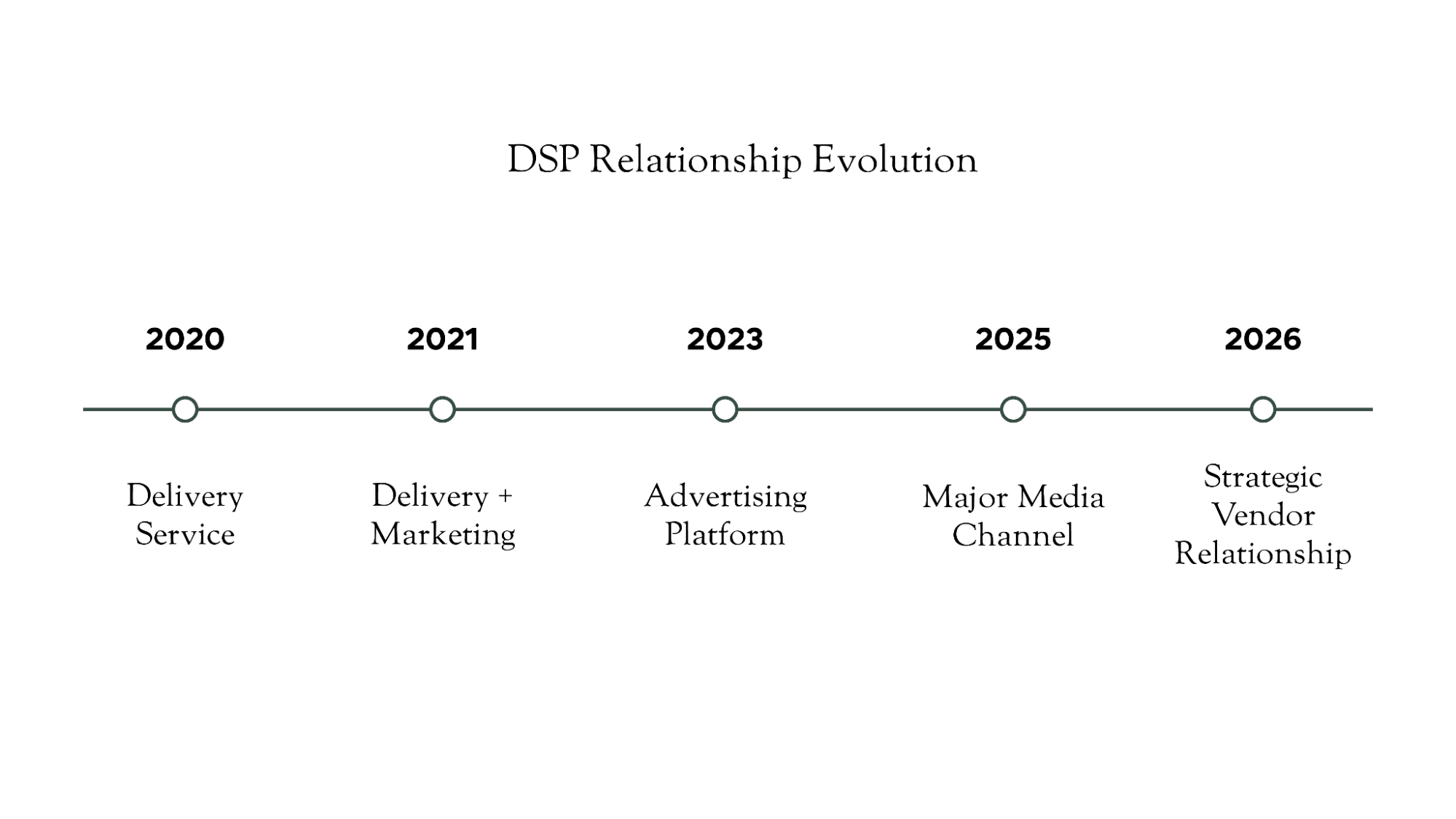

Consider this historical roadmap…

In 2020, a restaurant could be on a DSP, spend nothing beyond commission, and have solid visibility and discoverability. By 2021, paid advertising emerged as an opportunity for restaurants to drive more sales on the DSP platforms. By early 2025, DSP advertising had become a $2.5B industry5. The threshold for marketing spend on DSP platforms has moved from 0% to 5–6% to double-digit ranges in less than six years. And according to brand executives participating in a recent delivery roundtable, lack of participation at these levels of paid advertising results quickly in a volume penalty.

Marketing spend on a platform can be split between sponsored listings, paid search placements, promotions, and discounts - and each carries different economics. It is vital for brands to understand the difference between the forms of marketing spend and to dictate a deliberate strategy for investment into the platform.

Equally as hair-raising are special deals and offers for subscription members. In many cases, this equates to the restaurant effectively subsidizing the platform's guest retention program out of its own margin.

With the multitude of factors, terms, and rates now woven throughout DSP contracts, it is vital that brands understand the true total cost of their DSP platforms.

The Opacity Problem

The total cost of doing business on a DSP platform can include anywhere from six to eight separate expense categories: commission fees (regular and subscription), marketing fees (the cost of a guest redeeming a brand’s promo), delivery fees, marketing spend commitments, etc. Depending on the DSP, this can land the restaurant with a total cost (including the usual operating expenses) of 50% to over 100% of the value of the sale.

To exacerbate that confusion even more, each of the DSPs names these fees differently. When was the last time you read and completely understood a monthly statement from one of your DSPs?

The “headline" commission rate tells almost nothing about the effective cost of the service, yet many brands still focus solely on the commission rate as if it is the only number that matters. This leads to a tendency to underestimate the true cost of revenue on DSP channels.

The financial costs are only part of the story. Beyond margin, brands have quietly ceded something harder to recover: their guests.

Guest data is now a primary focus for brand leaders.

The Data Problem

Guest data is now a primary focus for brand leaders. The evolution of data tools and their ability to provide deep insights into purchasing behavior has been a game-changer for brand marketing and guest engagement.

For transactions that go through a DSP marketplace, that data (names, emails, order history, payment method) goes to the DSP. This means that many brand leaders are completely in the dark about the incrementality of DSP orders. Could that DSP order potentially be from brand-loyal guests who might otherwise order from them directly?

This problem is exacerbated by the brand's lack of agency to message to guests ordering through a DSP marketplace. DSPs control of guest data handcuffs brands that then lose insights into guest purchasing behavior to more effectively target marketing efforts and dollars.

Contract opacity and guest data omission are two practical challenges for brands managing their DSP partnerships. There is also a very relevant operational and industry factor that adds to the complexity of DSP management – it’s constantly changing.

The Nuance of the Shifting DSP Landscape

While the DSP partnership is part of everyday life for certain people on the brand side, DSP contracts renew every two to three years, the landscape they govern changes every six months. That gap is where brands get caught.

At the same time the DSP relationship and corresponding contract implications tend to change meaningfully every 6 months or so. Exchanging marketing spend for a reduction in commission rates was significant leverage less than a year ago; today, not so much. Some brands have been willing to allow for increases in marketplace commission rates to win reductions in subscription rates; that doesn’t always land anymore. What works as a strong lever in DSP negotiations today may be completely different by the end of this year.

Keeping current on the landscape is time-consuming, challenging, and largely disconnected from the normal course of running a restaurant business. So most brand leaders don't, and the DSP reps fill the void.

Coming Next…

The odds in DSP negotiations are not in brands' favor, and they're not getting better. But the brands that do well aren't the ones with the most leverage. They're the ones who show up prepared.

A clear strategy, critical analysis of current contract terms, scenario, and financial modeling, and a structured communication plan are all essential parts of the process. In Part 4 of our DSP series, which drops next week, we will cover how to succeed in creating a sustainable partnership with the DSPs.

1 https://www.deliverect.com/en-us/blog/trending/state-of-the-food-delivery-industry-in-the-us-2025

2 https://www.restaurantdive.com/news/uber-eats-increases-marketplace-fees/814294/

3 https://www.restaurantbusinessonline.com/technology/pie-five-owner-cuts-ties-uber-eats-after-fee-hike

4 https://www.sec.gov/Archives/edgar/data/1792789/000179278926000036/proddashex991-pressrelease.htm

5 https://https://www.restaurantbusinessonline.com/technology/discounts-are-reshaping-third-party-delivery-business

6 https://restaunax.com/blog/doordash-profitability-analysis

Ready to move? Let’s talk.